Authored by-Rodriquez Kjer

It's not always easy to get a home loan. Seeking out a mortgage that conforms to your budget can be a tricky. You have to know what you're looking for and have a lot of patience. Use the advice here to ensure you get the best rates for your mortgage.

If you know you want to apply for a home loan, get ready way before you plan on doing it. If you're thinking about purchasing a home, then you have to get your finances in order quickly. It means building a bit of savings and raising your credit score. Putting these things off too long can cause you to not get approved.

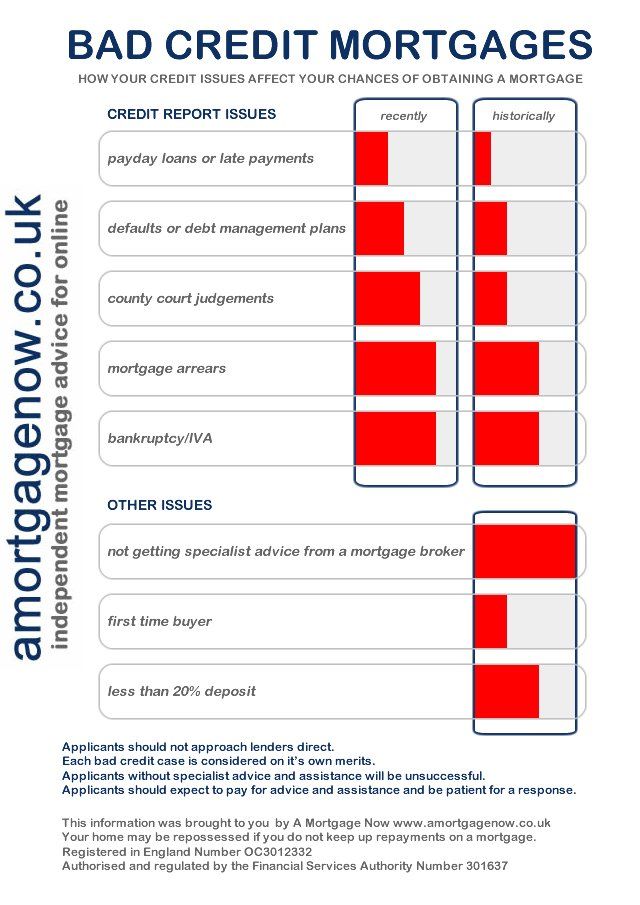

Know your credit score before beginning to shop for a home mortgage. If your credit score is low, it can negatively affect the interest rate offered. By understanding your credit score, you can help ensure that you get a fair interest rate. Most lenders require a credit score of at least 680 for approval.

You may wish to refinance without closing costs. You do not always need to spend your money to save money when you refinance. Many lenders will offer mortgages that have no closing costs. Lenders make up for these costs by charging you an interest rate that's slightly higher. This slight increase sometimes translates into some extra dollars in your monthly payment, but you can save thousands in your closing costs.

Be sure to communicate with your lender openly about your financial situation. Many homeowners may give up on their home because they do not understand that they still may have options to renegotiate it. Give the lender a call and tell them your situation.

Refinancing a home mortgage when interest rates are low can save you thousands of dollars on your mortgage. You may even be able to shorten the term of your loan from 30 years to 15 years and still have a monthly payment that is affordable. You can then pay your home off sooner.

Approach adjustable rate mortgages with caution. You may get a low rate for the first six months or so, but the rate can quickly increase to the current market rate. If the market rate goes up, your rate can go up as well. Just keep that in mind when you are considering that option.

Save up for the costs of closing. Though you should already be saving for your down payment, you should also save to pay the closing costs. They are the costs associated with the paperwork transactions, and the actual transfer of the home to you. If you do not save, you may find yourself faced with thousands of dollars due.

Be careful when taking out a second line of financing. Many financial institutions will allow you to borrow money on your home equity to pay off other debts. Remember you are not actually paying off those debts, but transferring them to your house. Check to make sure your new home loan is not at a higher interest rate than the original debts.

One type of loan that is not normally talked about is an interest only loan. This type of loan allows you to make low monthly payments for a certain period, then the payment amount increases. These loans are generally used to help you get into a home at a low monthly payment.

Stay persistent with your home mortgage hunt. Even if you have one lender rejects you, it doesn't mean they all will. Many tend to follow Freddie Mac and Fannie Mae's guidelines.

mouse click the next article may also have underwriting guidelines. Depending on the lender, these may stricter than others. You can always ask the lender why you were denied. Depending on the reason they give, you can try improving your credit quickly, or you can just go with a different lender.

Do not sign a home mortgage contract before you have determined that there is no doubt that you will be able to afford the payments. Just because the bank approves you for a loan does not mean that you could really endure it financially. First do the math so that you know that you will be able to keep the home that you buy.

Go online and use a mortgage calculator to find out how much of a loan you can afford. There are many sites that offer these free calculators. Additionally, there are

simply click for source that will tell you the final price you will be paying at the end of the loan and others that show how much you can save by paying extra toward the principal.

Avoid paying Lender's Mortgage Insurance (LMI), by giving 20 percent or more down payment when financing a mortgage. If you borrow more than 80 percent of your home's value, the lender will require you to obtain LMI. LMI protects the lender for any default payment on the loan. It is usually a percentage of your loan's value and can be quite expensive.

If you have less than perfect credit, one way to overcome it is to have a large down payment, more than most other borrowers. Although most people save up at least 5%, you should strive for 20% in order to help your approval chances.

Never assume that a good faith estimate is fact or written in stone. It is in fact not just an estimate, but one written in good faith. Always be wary of extra costs and fees that can creep into the official and formal paperwork later that drive up your total expense.

Consider a home mortgage plan that incorporates the property taxes into this. Some companies will even give you a break on interest if you do this, as in makes it more likely that you will keep possession of your home. Not paying your taxes could lead to someone else owning the property on which your home resides.

Look online for financing for a mortgage. You no longer have to go to a physical location to get a loan. A lot of reputable lenders have begun to offer mortgage services online, exclusively. They have the advantage of being decentralized and are able to process loans more quickly.

Most people would never get to live in their own home without a mortgage. Mortgages give you the chance to pay for your home while you enjoy it over many years. Still, that's a long time to live with that obligation, even after you went through the stress of getting the mortgage. Apply what you have learned from this article to minimize your mortgage stress.

icons at the top right corner of the subsection.

icons at the top right corner of the subsection.