Content writer-Niemann Kent

Home ownership is the American dream, but obtaining a mortgage loan in the current state of the economy can be difficult. There are multiple home mortgage options, and it is important that you choose the right one. This article contains some valuable tips to help you get a mortgage for the home you finally found.

Before getting a mortgage, study your credit history. Good credit is what can help you get a mortgage. Obtain copies of your credit history and scores from the three major credit-reporting bureaus. Study your reports carefully to ensure that no issues or errors must be resolved before you apply. Many lenders need a minimum score of 680, which complies with Freddie Mac and Fannie Mae's guidelines. Most lenders want to avoid scores that are lower than 620.

Prepare yourself for your mortgage application early. Your finances must be under control when you are house hunting. This ultimately means that you should have savings set aside and you take care of your debts. You may not get a loan if you wait.

Regardless of how much of a loan you're pre-approved for, know how much you can afford to spend on a home. Write out your budget. Include all your known expenses and leave a little extra for unforeseeable expenses that may pop up. Do not buy a more expensive home than you can afford.

Pay down your debt. You should minimize all other debts when you are pursuing financing on a home. Keep your credit in check, and pay off any credit cards you carry. This will help you to obtain financing more easily. The less debt you have, the more you will have to pay toward your mortgage.

Like most people, you will likely have to have some amount of money for a down payment. Some banks used to allow no down payments, but now they typically require it. Find out how much you'll have to pay before applying.

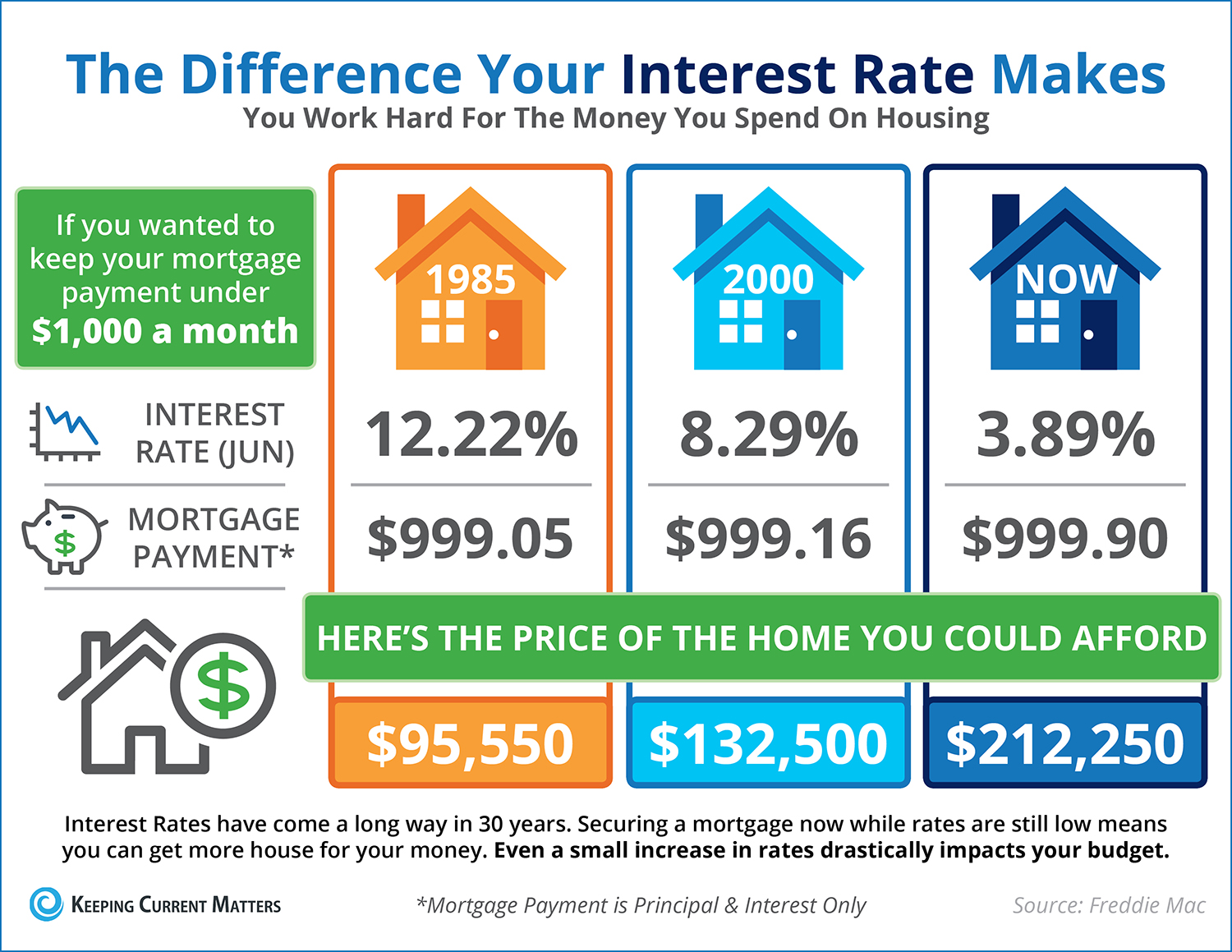

Find an interest rate that the lowest possible. Remember that it is in the best interest of banks to charge you a high interest rate. Don't let yourself be a victim of this. It is wise to shop around to many lenders so you have many choices to select from.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Read the fine print of your mortgage contract before signing. Many times home buyers find out too late that their fixed rate loan has a balloon payment tied to the end of the loan contract. By reading over the contract you can ensure that you are protected throughout the entire loan term.

Be careful when taking out a second line of financing. Many financial institutions will allow you to borrow money on your home equity to pay off other debts. Remember you are not actually paying off those debts, but transferring them to your house. Check to make sure your new home loan is not at a higher interest rate than the original debts.

If you are looking to buy any big ticket items, make sure that you wait until your loan has been closed. Buying large items may give the lender the idea that you are irresponsible and/or overextending yourself and they may worry about your ability to pay them back the money you are trying to borrow.

Read the fine print of your mortgage contract before signing. Many times home buyers find out too late that their fixed rate loan has a balloon payment tied to the end of the loan contract. By reading over the contract you can ensure that you are protected throughout the entire loan term.

Chose a bank to carry your mortgage. Not all companies who finance homes are banks. Some of them are investment companies and private corporations. Though you may be comfortable with them, banks are usually the easier option. Local bankers can usually cut down the turn-around time between application and available funds.

Be aware that certain things may need to be done to the property before the loan can be approved. One such thing is extra insulation added to the home.

Recommended Website can either be done by the home buyer or the homeowner. However, once the work is completed, it must be inspected by a certified inspector.

Before signing on the dotted line of your home mortgage, learn about the history of the property you are purchasing. There are many things sellers and lenders are not required to disclose that you might find relevant. knowing whether or not your new home was the scene of a gruesome murder might be something you want to know before agreeing to buy.

Do not embark on the process of buying a home if you have just started a new job within the last year. The best home mortgage rates go to those that have been with a company for a number of years. Having a job for a short time is seen as a risk, and you will be the one to pay for it with a higher interest rate.

Remember that interest rates are currently very low, and that means they can only go up from here. How would that impact your finances? Would you be able to afford them if they went up? If not, consider how large a mortgage you could afford in that situation instead.

Be

click the up coming website page when choosing a home. Just because your lender pre-approves you for a certain amount doesn't mean that's the amount you can afford. Look at your income and your budget realistically and choose a home with payments that are within your means. This will save you a lifetime of stress in the long run.

As you can see, there really is a lot to taking out a mortgage to buy a home. Don't let the feeling of being overwhelmed stop you, home ownership is wonderful. Just use the tips shared here and you can be on the right path to being a home owner.

icons at the top right corner of the subsection.

icons at the top right corner of the subsection.